:max_bytes(150000):strip_icc()/compoundinterest_final-5c67da5662ba458f8d9d229ab4ca4292.png)

Economic watchers are flagging a potential pause in interest rate hikes next month. This shift comes as recent data shows inflation numbers exhibiting a noticeable dampening effect. The central bank's typical levers, used to either stimulate or constrict economic activity through the cost of borrowing, appear poised for a period of stillness, rather than further escalation.

The current economic climate suggests a deviation from the aggressive monetary tightening seen recently, with a sustained drop in inflation figures being the primary driver for this anticipated inaction.

Understanding the Mechanics of Interest

At its core, interest represents the cost of borrowing money or the return on savings. It operates on two primary principles:

Simple Interest: This is calculated solely on the initial amount borrowed or saved, known as the principal.

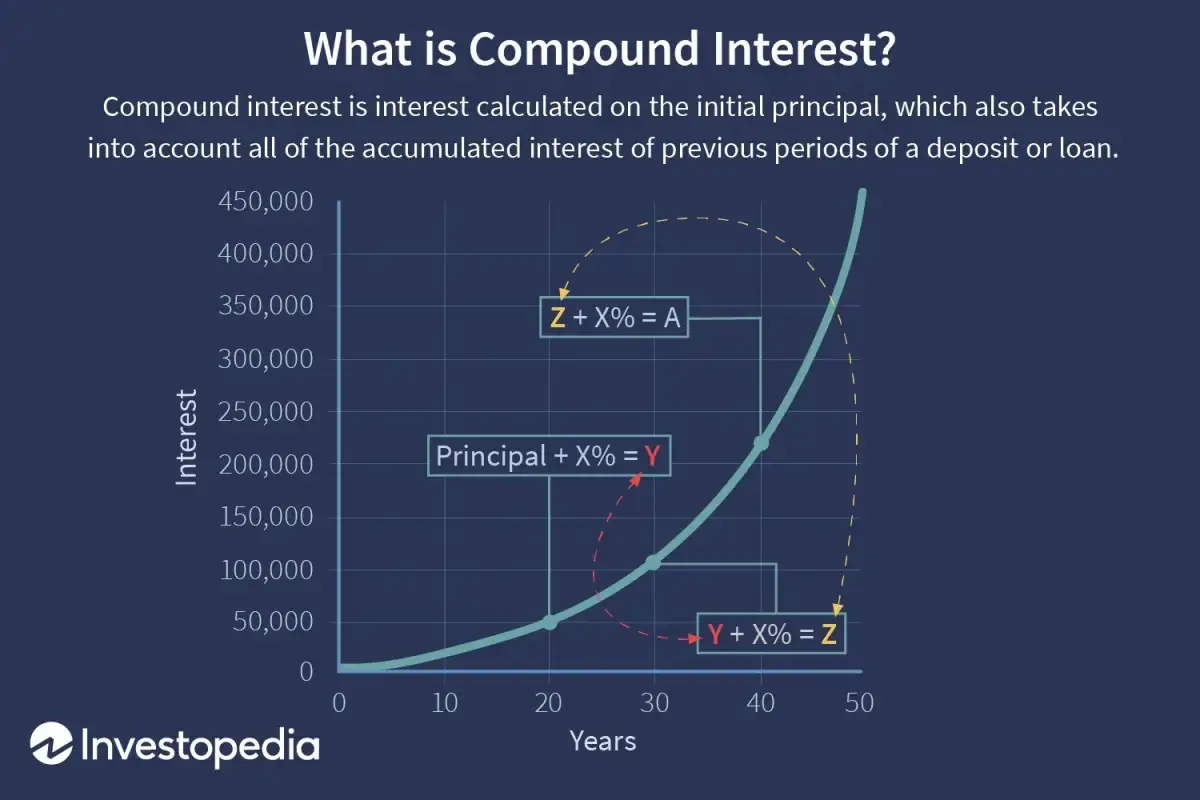

Compound Interest: A more potent force, compound interest means that earnings are calculated on the principal plus any interest that has already accumulated. This "interest on interest" effect can significantly amplify savings over time, a concept detailed in resources explaining compound interest mechanics.

Financial institutions, such as banks, employ these mechanisms to manage both loans and deposits. For savers, depositing money into accounts, particularly those offering higher yields, results in the accrual of interest. Conversely, for borrowers, interest adds to the total repayment amount of a loan. Tools like loan calculators can help estimate these future financial obligations.

Read More: San Francisco Meta worker earns $300k but has no car or couch

Financial Lexicon: A Glimpse

The language surrounding finance reveals a spectrum of interest-related terms. From a beneficial interest in legal contexts to the conflict of interest that can arise from opposing obligations, the concept permeates various domains. In finance, terms like controlling interest (indicating significant shareholding) and floating interest rate (a variable borrowing cost) are commonplace.

Other notable distinctions include:

Cumulative interest versus compound interest: While compound interest refers to earning interest on previously earned interest, cumulative interest is simply the sum of all interest payments over time.

Gross interest signifies the total accumulated interest, before any deductions.

An interest-free account, by definition, does not accrue any interest, while an interest-bearing account does.

The ongoing fluctuations in these rates are a subject of constant analysis and have far-reaching implications for both individual finances and broader economic stability.