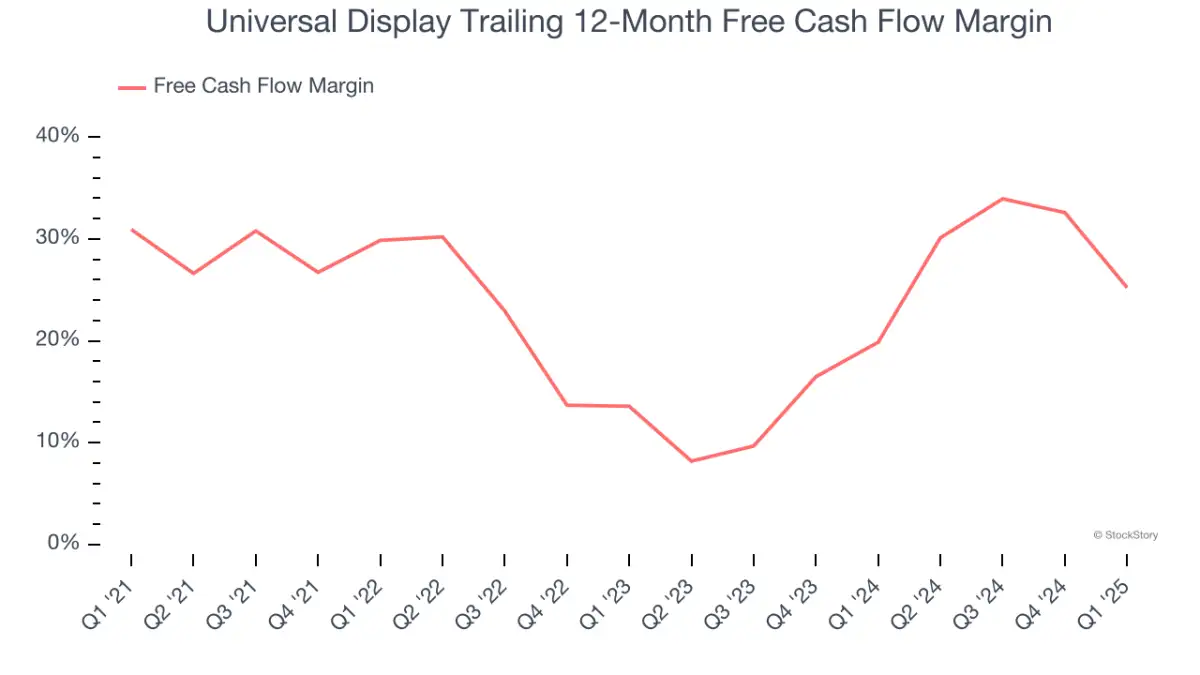

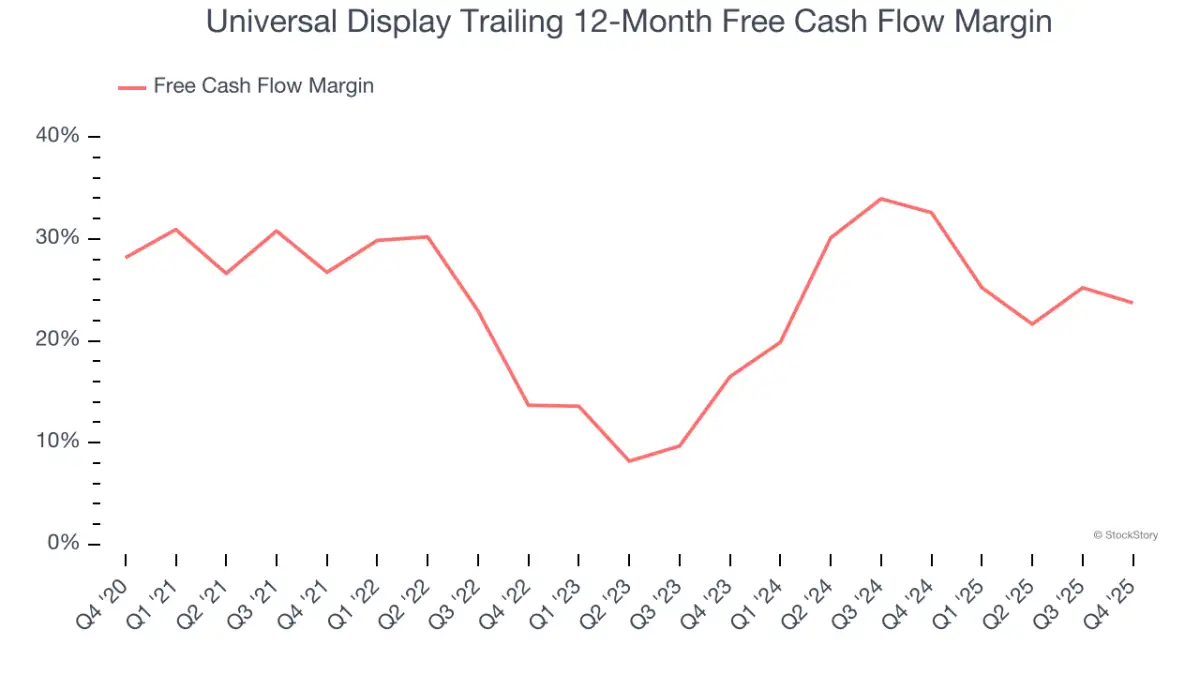

Concerns are surfacing regarding Universal Display (OLED), with specific critiques pointing to a diminishing free cash flow margin as a key indicator of its current business quality. This decline, highlighted by financial analysis firm 'StockStory', suggests that while the company might not be fundamentally flawed, its performance may not meet certain investor standards for growth or profitability. Despite recent price adjustments making the stock appear more accessible, the assessment leans towards recommending alternative investments that offer more robust financial metrics.

Declining Financial Signal

The core of the critique centers on the erosion of Universal Display's free cash flow generation. For observers who prioritize this particular metric – a measure of cash a company generates after accounting for capital expenditures – this trend is a significant red flag. The assertion is that Universal Display's business model, despite its technological contributions to the OLED market, exhibits a falling free cash flow margin, rendering it less appealing than other available opportunities.

This assessment appears to be a recurring theme across multiple reports, all referencing 'StockStory' as the source of the analysis. The firm, in its evaluations, has reportedly moved from a neutral stance to one of caution, advising investors to "swipe left" on Universal Display for the time being.

The Search for Alternatives

The narrative surrounding Universal Display is not just about its perceived shortcomings but also about the existence of potentially more lucrative avenues for investment. The underlying message from these reports is that superior investment choices exist, presenting a more compelling case for capital allocation than the current proposition offered by OLED. While specific alternative stock recommendations are offered elsewhere, the general sentiment is that a comparative analysis favors other market players.

Background on Universal Display

Universal Display Corporation is known for its development and commercialization of organic light-emitting diode (OLED) technologies and materials for use in displays and lighting. The company holds a significant intellectual property portfolio in this area. Its products are integral to the production of advanced display screens found in smartphones, televisions, and other electronic devices. The company's performance is often tied to the broader adoption and innovation within the OLED industry.

This critique emerges following the company's Q1 earnings report, an event that typically triggers a re-evaluation of stock prospects by market analysts and investors. The current analyses suggest that the post-earnings picture for Universal Display is less optimistic than might be desired by a segment of the investment community.